A shared, unchangeable ledger known as blockchain development is used by businesses to record transactions and track assets. Property, cash, real estate, and other tangibles are tangible investments (intellectual property, patents, copyrights, trademarks). Almost anything of value may be recorded and traded on a blockchain network, lowering costs and reducing risk for all parties.

A Web3 developer makes applications that aren’t confined to one cloud server but are allocated on a decentralized P2P network or blockchain that is not under the control of a single entity. In plainer terms, the planning, architecture, and security of blockchain systems are handled by a web3 developer.

Why blockchain is important

The blockchain development company is using cutting-edge technology that may eliminate fraud, lower security concerns, and increase transparency in a scalable manner. The association of blockchain technology with cryptocurrencies and NFTs helped it acquire popularity, and it has subsequently developed into a management solution for all international businesses.

Currently, blockchain technology is preserving healthcare data, creating cutting-edge games, bringing transparency to the food supply chain, and radically altering how data and assets are managed.

Key features of a blockchain

- Distributed ledgers

The distributed ledger and its immutable transaction records are available to all network users. Transactions are only recorded once with this shared ledger, preventing the redundancy of effort seen in conventional corporate networks.

- Immutable records

Nobody can tamper with or change a transaction once it has been added to a shared ledger. Correct errors must be corrected by adding a new trade in the transaction record. Following that, what can be seen are both transactions.

- Smart contract

A collection of guidelines known as Smart contracts are saved on the blockchain development services and automatically carried out to speed up transactions. The conditions of a bond transfer or the terms of payment travel insurance can be specified in a smart contract.

Benefits of blockchain

- Increased assurance

By using blockchain development solutions, you can be sure that as a user of a member-only network, you will always receive up-to-date information and that private blockchain records will only be shared with network users who have explicitly authorized access.

- Greater security

All network participants must concur that the data is accurate and all verified transactions are permanently stored and unchangeable. Even system administrators are unable to remove transactions.

- More effective

A distributed ledger maintained across network participants eliminates the requirement for time-consuming record reconciliation. Additionally, the blockchain can store and automatically execute smart contracts, which are collections of rules, to speed up transactions.

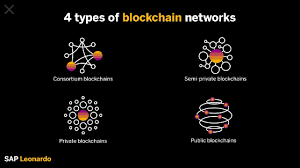

Types of blockchain networks

- Public blockchain network

Anybody can enter a public blockchain, which anyone can access. For instance, bitcoin. There are drawbacks to significant processing power requirements, little to no transaction privacy, and lax security. For blockchain enterprise use cases, these are crucial factors to consider.

- Private blockchain networks

A decentralized, peer-to-peer, private blockchain network is similar to a public blockchain network. The consensus mechanism, shared ledger, network, and participation rules are all controlled by a single organization.

Relying on the application can significantly increase participant trust. Private blockchains can be hosted locally and run behind company firewalls.

- Permissioned blockchain networks

Permissioned blockchain networks are often set up by businesses that create private blockchains. It’s significant to remember that open blockchain networks might be permitted. Due to these restrictions, only certain users and types of transactions are allowed on the network. To join, participants must be invited or given permission.

- Consortium blockchains

The upkeep of a blockchain might be divided among several businesses. Who can nominate these pre-selected companies to decide on transactions and have access to data? In a consortium blockchain, each partner must approve the blockchain and share ownership of it. In some situations, it’s ideal.

{kind=link}